Business owners often devote years to building their company, yet give far less attention to what happens to that business if they die or become incapacitated. Many assume the business will simply continue, be sold, or be dealt with “through the estate.”

Navigating corporate succession requires far more than a standard personal Will. Proactive estate planning for business owners is the only reliable way to ensure your company survives a tragedy, your family is shielded from heavy tax burdens, and your legacy isn’t lost to probate delays or a forced liquidation sale.

In this guide, we will break down exactly what happens to a business when an owner dies in Alberta, from the legal paralysis of corporate authority to the complexities of Unanimous Shareholder Agreements (USAs), and outline the critical steps you must take today to protect your life’s work.

How Alberta Law Handles Business Assets

Most assets in an Alberta estate can be collected, valued, and ultimately distributed to beneficiaries once the executor has obtained the necessary legal authority. A privately owned business is different.

Although a corporation’s shares and partnership interests form part of the deceased’s estate, the business is also an active enterprise with legal, financial, and operational responsibilities that continue regardless of the owner’s death. Alberta’s probate and estate laws determine how ownership interests are administered, but they do not eliminate the separate legal rules that govern how a business is managed.

As a result, business assets often require significantly more planning, coordination, and legal oversight than other estate property.

Some of the key ways a business differs from other estate assets under Alberta law include:

- Ownership and management are separate legal concepts

The executor may eventually gain authority over the deceased’s ownership interest through the estate administration process, but that does not automatically give them authority to manage the corporation’s daily operations or make corporate decisions.

- Corporate law continues to apply

Even after the owner’s death, the corporation must continue complying with its governing documents, shareholder agreements, applicable corporate legislation, tax obligations, employment laws, and contractual commitments.

- The business cannot simply be “distributed.”

Unlike cash, vehicles, or personal belongings, a business often must continue operating while the estate is being administered. The executor may need to preserve its value, oversee management, or prepare it for sale before beneficiaries receive their inheritance.

- Probate may be only one step in the process

A Grant of Probate confirms the executor’s authority to administer the estate. But additional corporate actions, such as appointing directors, updating shareholder records, or changing signing authorities, may still be required before the business can operate normally.

- The value of the asset can change rapidly

A business is a dynamic asset whose value depends on ongoing operations, customer relationships, employees, contracts, and cash flow. Delays in decision-making during estate administration can directly affect the company’s financial performance and the value ultimately available to beneficiaries.

- Employees, creditors, and customers have continuing rights

The death of the owner does not suspend payroll obligations, supplier contracts, tax filing deadlines, lease payments, or customer commitments. These responsibilities continue while the estate is being administered.

- Business succession often requires additional legal planning

Wills, shareholder agreements, buy-sell agreements, corporate minute books, powers of attorney, and tax planning should work together. If these documents are not coordinated, the estate administration process can become significantly more complex and may delay the transfer, continuation, or sale of the business.

The Executor’s Authority Has Limits

Many executors assume that once they are named in a will, they immediately gain full control over the assets owned by the deceased. In reality, corporate assets are governed by both estate law and corporate law.

Under Alberta’s legislation, an executor derives authority from the will and, where necessary, from a Grant of Probate, but that authority does not automatically allow the executor to assume the operational role previously held by the deceased.

Corporate governance documents, shareholder agreements, banking requirements, and applicable legislation may all affect how control of the company is transferred.

If the deceased was the sole director, sole shareholder actively managing the business, or the only person authorized to sign banking documents or enter into contracts, the corporation can become effectively paralyzed until appropriate corporate steps are completed.

Routine business decisions may be delayed, financial institutions may restrict account access, and contracts requiring authorized signatures may be placed on hold.

Depending on the business structure, new directors may need to be appointed before the executor can effectively manage the corporation’s affairs.

Without a succession plan that coordinates estate documents with corporate governance, even a financially healthy company can experience unnecessary disruption. Careful planning before death and prompt legal guidance after death can help ensure the business continues operating while protecting both its value and the interests of the estate’s beneficiaries.

| Stage After Death | What Typically Happens | Potential Impact on the Business |

| Business owner dies | Day-to-day leadership immediately stops. | Operations may continue, but decision-making authority can become uncertain. |

| Executor begins estate administration | Will is reviewed, and probate may be required. | Executor gains estate responsibilities but may not yet have practical corporate control. |

| Corporate authority is assessed | Directors, shareholders, signing authorities, and corporate records are reviewed. | Banking, contracts, and operational decisions may be delayed if no replacement authority exists. |

| Corporate governance steps completed | New directors or authorized representatives are appointed where permitted. | The business can resume normal governance and operational decision-making. |

| Long-term succession decisions are made | Business may continue operating, be transferred to family members, or be sold. | Proper planning helps preserve business value and protect beneficiaries’ interests. |

The Importance of Shareholder Agreements

For business owners with partners or shareholders, a shareholder agreement is often the most important document governing what happens on death.

Well-drafted agreements typically address:

- What occurs if a shareholder dies, including whether shares must be sold

- Who can purchase shares

- How shares are valued

- How the purchase is funded

Without such provisions, surviving shareholders and the estate may be left negotiating under pressure, with conflicting interests and limited guidance.

In the absence of clear terms, disputes are far more likely.

Family Businesses Add Another Layer of Complexity

Family businesses often create unique estate administration challenges because family relationships, business operations, and inheritance goals frequently overlap.

While one child may have spent years working in the business and expect to continue running it, other beneficiaries may expect an equal share of the estate despite having no involvement. Under Alberta law, an executor has a fiduciary duty to act impartially and in the best interests of all beneficiaries, making these situations particularly complex.

Without a coordinated succession plan, probate, business operations, and family expectations can quickly come into conflict, increasing the risk of disputes, delays, and a loss of business value.

Common challenges include:

- Different levels of family involvement

Some beneficiaries actively manage the business while others have never participated.

- Fairness versus equality

Dividing ownership equally is not always the fairest or most practical solution.

- Business valuation disputes

Professional valuations are often needed to determine each beneficiary’s entitlement.

- Maintaining operations during probate

Payroll, contracts, taxes, and customer obligations continue while estate administration continues.

- Corporate succession issues

New directors or signing authorities may need to be appointed before the business can operate normally.

- Conflicts over the future of the business

Beneficiaries may disagree on whether the company should be sold, transferred, or continue operating.

- Tax and succession planning

Coordinating wills, shareholder agreements, and corporate records can help preserve the business and reduce future disputes.

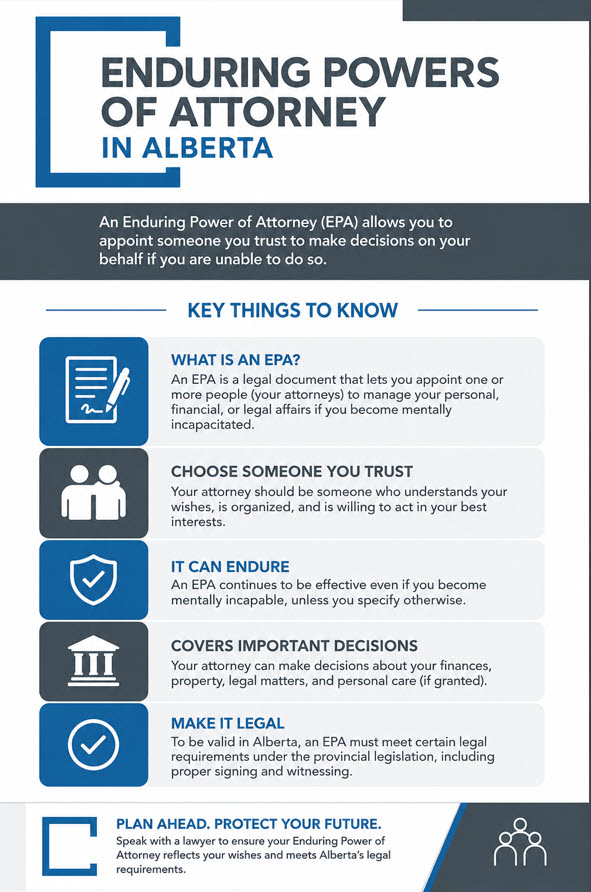

Addressing Incapacity with an Enduring Power of Attorney

Estate planning for business owners should also address incapacity. If an owner becomes unable to manage their affairs, someone must be legally authorized to make decisions.

A properly drafted Enduring Power of Attorney, coordinated with corporate documents, can allow trusted individuals to manage business interests during incapacity.

Without this planning, court applications may be required, causing delays and uncertainty at a critical time.

Integrated Planning Protects the Value of Your Business

Effective planning for business owners involves aligning corporate documents, shareholder agreements, and estate planning documents so they work together.

This integrated approach helps ensure that:

- The business can continue operating

- Executors have clear authority

- Beneficiaries understand what to expect

- Value is preserved rather than eroded

Planning does not need to be complicated, but it does need to be intentional.

Safeguard the Future of Your Business with an Estate Planning Consultation with Bosecke LLP

For business owners, estate planning is the process of ensuring continuity, protecting value, and reducing disruption for those left behind.

Without proper planning, a business can quickly become a source of delay, conflict, and financial loss during estate administration. With the right legal structure in place, it can remain one of the estate’s strongest assets.

If you own a business and have not reviewed how it fits into your estate plan, the team at Bosecke LLP would be pleased to help you develop a plan that protects both your business and your legacy. Schedule your free consultation today with our estate planning lawyers.